overview

Although economic indicators such as inflation, interest rates and stock markets went up and down, SSPF achieved a positive investment result of 6.7%.

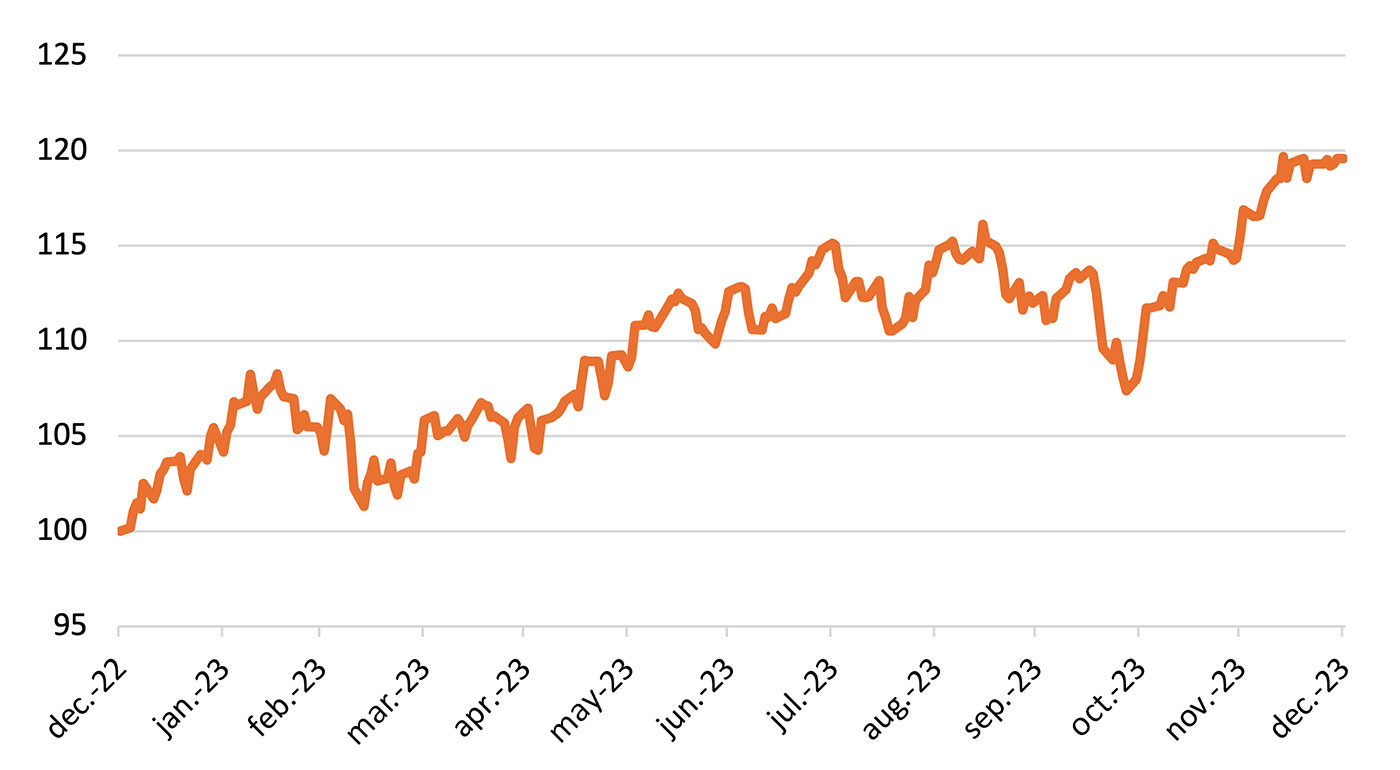

Dutch inflation, which was historically high in 2022, showed a declining trend in 2023. The decline in inflation was largely due to significantly lower energy prices in 2023 compared to 2022. Not only did inflation rates decline in the Netherlands but also in the United States and other European countries. Investors became more confident that inflation would eventually return to 'normal' levels. As a result, central banks will have room to cut interest rates in 2024. All this led to a strong final sprint in the stock markets in the last 3 months of 2023. Throughout 2023, stock markets generally showed a positive price trend (see Figure 1).

Figure 1: Trends in developed market shares (MSCI World Total Return Index in euro). Source: Bloomberg

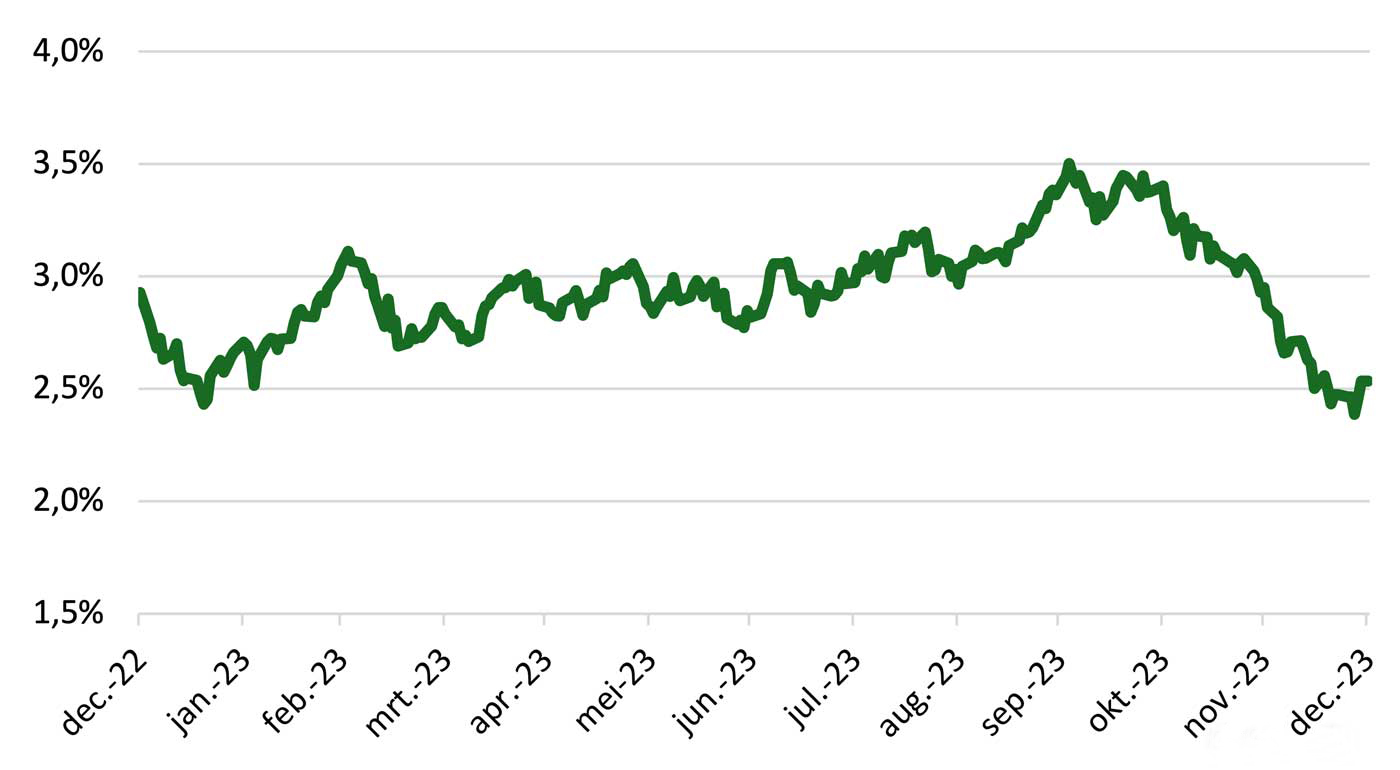

Due to rapidly rising global inflation in 2022, entities such as the US Fed (Federal Reserve), the Bank of England, and the European Central Bank intervened in the interest rate market. This trend continued into 2023, with central banks raising policy interest rates several times. The aim of these interest rate hikes was to slow down the economy to mitigate inflation. For instance, the 20-year euro swap interest rate was still 2.9% at the beginning of 2023 and rose to 3.5% by early October 2023. In the last 3 months of 2023, the interest rate market turned around. Investors became increasingly confident that inflation had indeed slowed down and that central banks would not raise policy rates again. Consequently, the 20-year euro swap interest rate fell sharply in the last quarter and ended at around 2.5% by the end of 2023 (see also Figure 2).

Interest rate effect on pension fund

Overall, interest rates decreased throughout 2023. A decline in interest rates is generally less favourable for a pension fund. A lower interest rate implies that the pension fund needs more funds in reserve to cover pensions. As the pension fund partially hedges interest rate risk with the Matching portfolio, a fall in interest rates often results in a positive investment outcome, limiting the impact of interest rate movements on the funding ratio.

Figure 2: Trends in interest rates (20-year euro swap rates). Source: Bloomberg

Due to the sharp drop in interest rates and the strong year-end performance of return-seeking assets in the fourth quarter, nearly all asset categories achieved positive returns. Consequently, the pension fund concluded 2023 with a positive return of 6.7%. With this performance, the pension fund outpaced the benchmark by 0.6%.

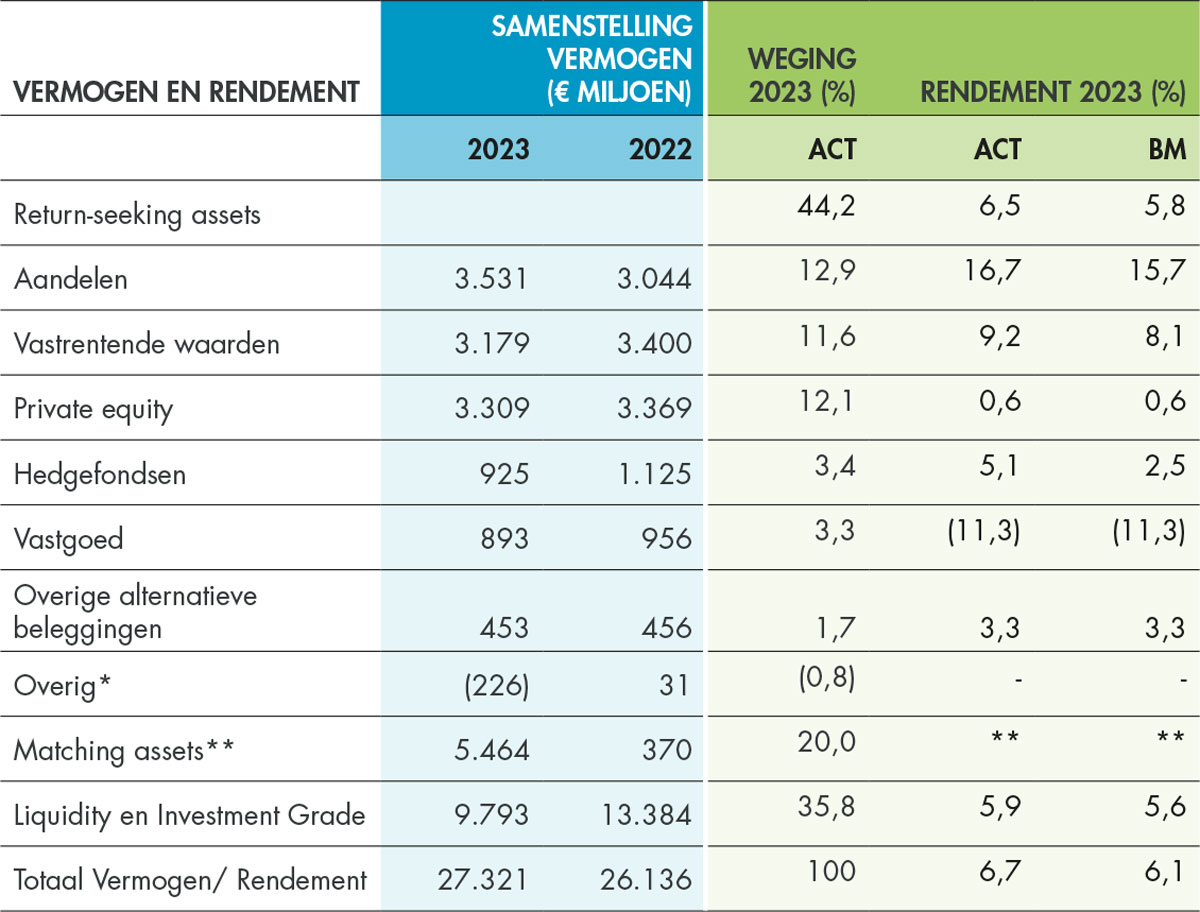

The table below shows the assets and returns of SSPF's1 investment portfolio. The table divides the total portfolio into 3 sub portfolios and compares the achieved returns with the benchmarks set by the board.

In 2023, the decreased interest rates led to an increase in value of the Matching assets, which largely consist of interest rate swaps. 2022 was a year marked by a historic rise in interest rates. This had a negative impact on the value of interest rate swaps. Additionally, the real hedge was enhanced in 2023, resulting in an increase in the Matching assets and a decrease in the Liquidity and Investment Grade portfolio.

Figure 3: Development of developed market shares (MSCI World Total Return Index in euros).

Source: Bloomberg

* Includes, among others, cash, cash equivalents and currency swaps, for which the performance and benchmark are not determined.

** The matching assets subportfolio holds derivatives, as a result of which a return reflected as a percentage cannot be adequately represented. The return in euro of this portfolio in 2023 is €527 million (versus the benchmark €449 million).

[1] This includes derivatives per investment category. Derivatives are presented as a separate balance sheet item in the annual accounts, which are based on reporting rules from Title 9, Book 2 of the Dutch Civil Code and International Financial Reporting Standards (IFRS), whereby 'receivables' are not offset. As a result, the asset composition in the table above differs from the presentation in the annual accounts.